For years, China’s real estate market has been growing massively. But over time the real estate boom seems to have turned into a bubble. More and more people started noticing how a lot of high-rise complexes and even whole neighbourhoods stay empty.

Like this map and want to support Landgeist? The best way to support Landgeist, is by sharing this map. When you share this map, make sure that you credit Landgeist and link to the source article. If you share it on Instagram, just tag @Land_geist. On X / Twitter tag @Landgeist.

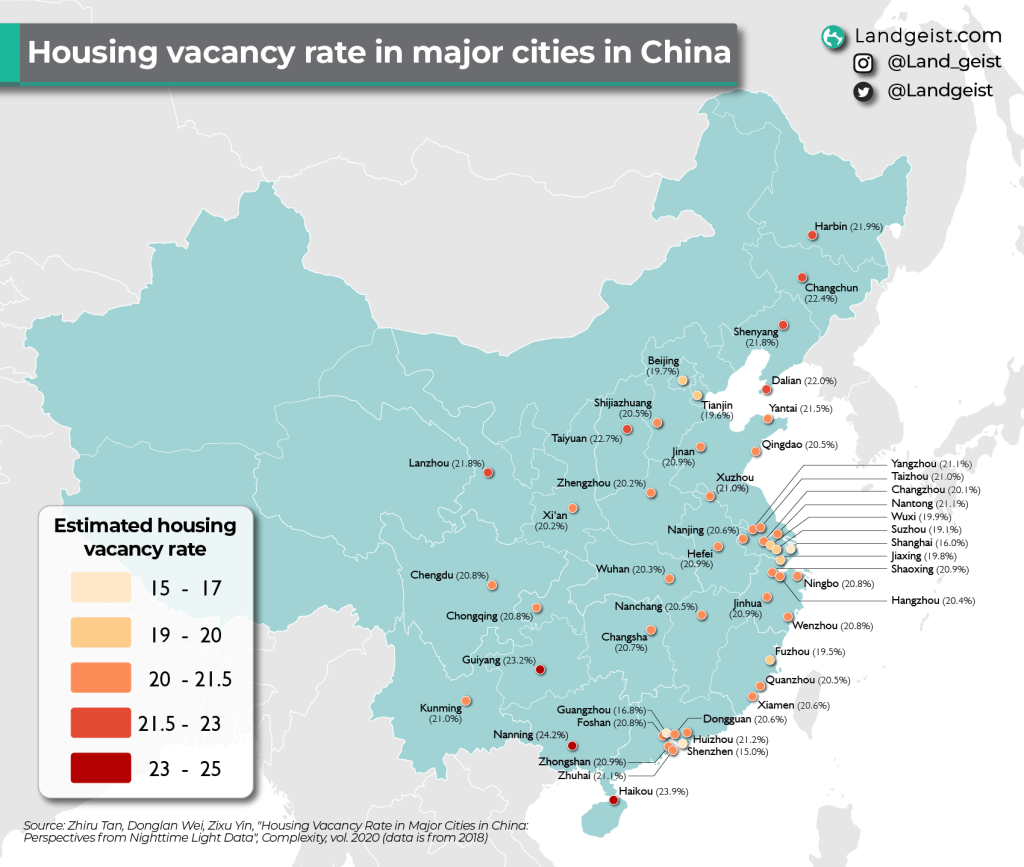

Sadly, the Chinese government is very opaque when it comes to statistics. Statistics on vacancy rates in China are more or less non-existing. However, a study has been done to estimate the vacancy rate in China’s major cities by looking at night-time light data.

This map shows the vacancy rate for China’s tier 1, new tier 1 and tier 2 cities. These are China’s biggest and most developed cities. As we can see, the vacancy rate ranges from 15% in Shenzhen to 24.2% in Nanning. Tier 1 cities like Shenzhen and Shanghai have the lowest vacancy rates, however, this is still very high. The highest vacancy rate can be found in China’s north-east and in inland cities, like Harbin or Guiyang. The housing vacancy rate is also highest in tier 2 cities, compared to tier 1 and new tier 1 cities.

As this study only looks into China’s major cities, there is a good chance that several lower tier cities have an even higher vacancy rate.

For comparison, the housing vacancy rate in major US cities is mostly below 10%. The Miami metro area is the highest of all US cities with 16%. In New York it’s 9.3%, Chicago 8.6% and San Francisco 5.9%. In Australia it’s even lower. Melbourne has a housing vacancy rate of 3.5% and Sydney 2.7%. In Tokyo, the dwelling vacancy rate (which includes more than just houses), is 10.6%.

Empty apartments, but most have an owner

The interesting thing is, that although these apartments are vacant, most of them do have an owner. But the majority of these owners have no intention of ever moving in, let alone renting them out. They intend to keep them vacant, as these apartments are an investment. Many Chinese believe that renting out their apartment will lower the apartment’s value. A lot of the home buyers in recent years, already own one or multiple homes. In 2018 for instance, 87% of new home buyers already owned at least one home.

China has a weak social security system, forcing people to save for themselves and supplement or even fund their own pension. Many families have even invested the savings of multiple generations into real estate. Real estate is one of the few investment options that Chinese people consider to be safe. Especially after the stock market crash in 2016, Chinese people have turned even more to the real estate market. To the point where Chinese have become obsessed with real estate. 75% of household wealth in China is in real estate.

Real estate isn’t just popular for investment. A significant portion of home buyers in China, are young men looking to get married. Men need a house to get married. The future bride and her family, often expect her future groom to own a house in order to get married. This is partially caused by the surplus of men caused by the one-child policy. This has given a lot of Chinese women the opportunity to be picky about her future husband, even in terms of material things.

Soaring property prices

Despite all the empty apartments, real estate prices keep soaring. Making it almost unaffordable for young Chinese to rent or buy a home to live in, especially in the big cities. In many major Chinese cities, it takes more than 25 annual salaries to buy a median sized apartment. In cities like Beijing or Shenzhen this is even over 40 years. For comparison, in New York one needs 9 annual salaries to buy a median apartment. In London this is 13 and in Tokyo 14.

The obsession with real estate has gotten to the point now, where homes are already sold before construction starts. Sometimes even years in advance. Heavy down-payments, sometimes more than 70%, are not uncommon. These pre-sales are almost like a Ponzi scheme, but have been a creative way for real estate developers to get more funding.

Slowing urbanization and the demographic crisis

You could argue that these houses are built for all the people from the rural areas that would move to the bigger cities in the future. Well, that is most likely not the case. China’s Hukou system makes it very difficult for people from rural areas to move to the big cities. They need a visa/permit to be able to move to a city. There are however still a lot of so-called migrant workers from China’s rural areas that live and work in the big city. However, they are officially still registered in their hometown in the countryside. Which means that they have only very limited access to the services in that city. Their children still live in their hometown, as they can’t access the schools in the cities that their parents work in. They also have to go back to their hometown whenever they need medical treatment for instance.

But the migration rate of people from rural to urban areas in China has been slowing for almost 2 decades and more and more of them return to the country side because they can’t find a job. On top of that, China is facing a demographic crisis. Its population is expected to shrink in the near future (some experts believe it already is). The 20 to 50 year-old demographic segment, is the most important target group for buying homes. This demographic segment will only decrease in the coming years and decades. Demand for housing (to live in), is only going to decrease in the future.

Considering the above, in combination with the short life expectancy of the buildings, combined with the massive over-supply. It is likely that only in a few cities the demand for housing (to actually live in, not as an investment) will catch up with the large supply. This becomes especially clear when we look at how local governments generate revenue and meet their GDP targets. The real estate boom has little to do with making sure there is enough housing for the future.

Land sales and tax revenue

With Evergrande, and most likely many other major Chinese real estate developers, in dire straits, there looms an even greater danger. If the real estate market would crash, this could cause the Chinese government to miss out on a lot of revenue. On top of that, it will also lower China’s GDP growth (and therefore the Chinese economy) significantly, which can be a real threat to Xi Jinping or even the CCP’s grip on power. To understand this a bit better, we need to dive in a bit deeper and get a sense of how the Chinese real estate boom/bubble started.

To understand this, we need to first look at how the Chinese government funds it expenses and distributes its tax revenue. Local and provincial governments are responsible for funding 80% of the Chinese government’s expenses. However, they only receive about half of all the tax revenue. The rest goes to the national government. This has forced the provincial and local governments to find creative ways to fund their expenses.

One of the resources that provincial and local governments have that can be profited from with little to no initial costs, is land. The Chinese government owns all land in China, so it’s an almost infinite resource for provincial and local governments. Land sales account for about 30% of provincial and local government income. But you have to be aware that buying land or a house in China works a bit different than in other countries. When you buy a house in China, unlike most countries, you don’t actually own the land it stands on. Instead, you get a 70-year lease from the government.

Apart from land sales, there is another important source of income: tax revenue. Selling the land to development companies creates a lot of economic activity. All the companies that are involved in the construction of these real estate developments, bring in a lot of tax revenue for the government.

Local governments have been known to use local government financing vehicles to take out bad loans for so-called ‘zombie companies’. A zombie company is a company that is technically bankrupt and doesn’t make any profit any more. Although they don’t make a profit, they still sell their products, on which they have to pay value-added tax. Some local governments are so desperate for that tax revenue, that they keep these companies alive by giving them loan after loan. This will create massive problems in the future, as these companies will never be able to pay back those loans, meaning the loans go bad. A lot of the debt of both these companies and the local government is hidden in these local government financing vehicles. Even premier Li Keqiang has acknowledged this problem.

It is estimated that 40% of the bank loans in China are from real estate developers or related companies. Economists have estimated that 15% of all bank loans in China have turned bad.

GDP targets that encourage unsustainable economic growth

On top of finding ways to fund their expenses, local governments also have GDP targets they need to meet. If they don’t, then they risk being fired or miss out on a promotion. Local government officials will therefore do anything to pump up GDP numbers. It’s been suspected for a long time that China’s GDP numbers are overinflated due to local government officials cooking the books to meet the GDP targets.

But there are also real ways in which the GDP growth is realised. A lot of it comes from real estate development. Which accounts for 15% of China’s GDP. Keep in mind that the real estate boom doesn’t just benefit real estate developers. There are a lot of industries like construction, steel, concrete, infrastructure etc. that benefit from it. On top of that, a lot of China’s large banks are heavily dependent on mortgages. If you add these up to the GDP numbers, then real estate accounts for 30% of China’s GDP. For comparison, at the height of America’s housing bubble, real estate account for only 18% of the US’s GDP. It is clear that a significant part of China’s economic growth is from unsustainable growth in the real estate sector.

But this hunger for tax revenue and GDP growth has also affected the quality of the buildings. Companies and governments rush to put up as many apartment buildings as quickly as possible. Corners are cut by using cheap low-quality materials and governments sometimes look the other way due to corruption. The average house in China has a life expectancy of 25-35 years, where 75-100 years or even longer is the norm in the US and Europe.

Will the bubble burst with a big bang?

As you can see, in China, both the people and the government, have become addicted to real estate. It has created an unhealthy real estate bubble. One day, this bubble will burst. The Chinese government has the power to postpone the bursting of the bubble almost infinitely, almost. Every time they kick the can down the road, the bubble gets bigger and therefore the crash will be harder. But every time they kick the can down the road, they can kick it less and less far. Instead of planning ahead and avoiding the bubble from getting too big, the CCP has decided to ignore it and even keep feeding it. An authoritarian government’s primary goal is to stay in power, which often leads to ignoring the problem or solving it with short term solutions, that only create bigger problems further down the road.

It is unlikely that this bubble will burst with a big bang. It will most likely be a slow and long pop. Chances are big that the real estate market crash in China will have similar effects to the one in Japan in the 1990s. Especially because China is growing old before they get rich, they could face years or even decades of little to no economic growth.

A real estate crash poses a lot of existential threats to the CCP and Xi Jinping. China’s economy, banking system and government revenue are heavily dependent on the real estate sector. Many jobs, but also people’s retirement is at risk. Banks might be left with bad loans worth trillions of dollars. The wealthy and powerful of China might threaten Xi and the CCP’s power, as they have most of their wealth tied up in real estate. But the biggest victims are the Chinese people, who might see their hard-earned life-time savings and pension disappear.

As you can see, this article is far longer than most of my previous articles. Sometimes there are subjects that fascinate me and I love reading up on it and take myself down into a rabbit hole. China and East Asia in general is a part of the world that I absolutely love. The information in this article is based on a lot of information and books that I’ve read over the past years about China and its economic and political system. If you are curious to read more about China’s real estate market or the challenges that China is facing at the moment, I highly recommend the following books (that I also used as sources for this article):

- China’s Great Wall of Debt by Dinny McMahon

- China the Bubble That Never Pops by Thomas Orlik

- Red Flags: Why Xi’s China is in Jeopardy by George Magnus

If you don’t feel like reading, have a look at this insightful video by PolyMatter about China’s Housing Crisis.

Leave a comment